Not every company that wants to go public is ready for the big leagues. That’s exactly the gap a Growth Enterprise Market is built to fill.

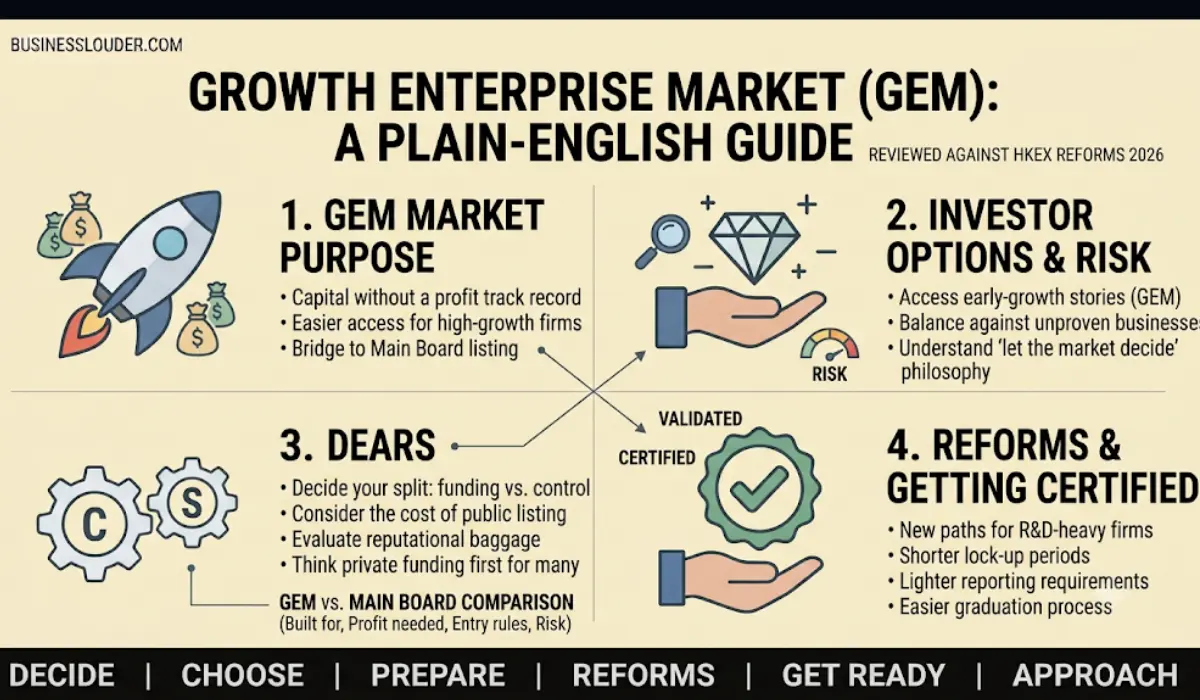

A Growth Enterprise Market — often shortened to GEM — is a junior stock exchange board designed for smaller, younger, high-growth companies that can’t yet meet the strict requirements of a main stock market. Think of it as the stock market’s minor league: a place where a promising company can raise money from public investors before it’s big or profitable enough for the main board.

If you’re a founder eyeing growth capital, or an investor wondering why some listed companies sit on a separate board, this is the piece that explains it in plain English — the good, the risky, and what’s actually changing.

What is a Growth Enterprise Market, really?

Every major stock exchange has a “main board” — the premier league where the big, established companies list. To get there, you usually need a track record: years of profit, a certain size, a clean financial history. Most young companies simply don’t have that yet.

So exchanges created a second tier. The most well-known is the Hong Kong Stock Exchange’s GEM, which launched in 1999 specifically, in its own words, for “growth companies that do not fulfill the requirements of profitability or track record for the main board.” London has its own version — the Alternative Investment Market, or AIM. Kenya’s Nairobi exchange runs a Growth Enterprise Market Segment. Different names, same idea.

The trade-off baked into these markets is simple: easier access in exchange for more risk. The company gets to raise capital sooner. The investor gets earlier access to a growth story — and takes on the danger that comes with a younger, unproven business. GEM runs on a “let the market decide” philosophy, leaning on heavy disclosure rather than the exchange vouching for whether the business will actually work.

Growth Enterprise Market vs. the Main Board

| Growth Enterprise Market (GEM) | Main Board | |

|---|---|---|

| Built for | Smaller, younger, high-growth firms | Large, established companies |

| Profit / track record | Not required | Usually required |

| Entry requirements | Lower | Higher |

| Investor risk | Higher | Lower |

| Liquidity | Often thinner | Deeper |

Why would a company list on a Growth Enterprise Market?

Because raising money is oxygen, and the main board door is often closed to companies that need it most.

Here’s what a GEM listing offers a growing business:

- Capital without the profit gate. You can raise public money before you’re profitable — the exact stage when many companies need it most.

- Lower entry requirements. The financial thresholds are gentler than the main board’s, so smaller companies actually qualify.

- A stepping stone. A GEM listing can be a launchpad. Prove yourself there, and you can graduate to the main board later.

- Visibility and credibility. Being publicly listed — even on a junior board — raises your profile with customers, partners, and future investors.

To put a real number on it: since the Hong Kong GEM opened in 1999, more than 267 companies have raised over HKD 40 billion through it, according to the exchange’s own figures. That’s real capital reaching real growth-stage companies that the main board would have turned away.

Deciding whether to list at all is a major strategic call, not a financing detail — the kind of choice that deserves a proper decision-making process rather than a gut reaction to a banker’s pitch.

The honest downside nobody puts in the brochure

Here’s where most explainers go quiet. Growth Enterprise Markets have struggled — and pretending otherwise would do you a disservice.

The same features that make them accessible also make them riskier. Younger companies fail more often. Trading volumes on junior boards are often thin, meaning it can be hard to buy or sell shares without moving the price. And over the years, some GEM boards developed a reputation problem — seen by parts of the market as a home for speculative or low-quality listings rather than tomorrow’s blue chips.

The numbers reflect it. Hong Kong’s GEM saw new listings and capital raised decline sharply after 2019, to the point that regulators had to step in and overhaul the rules. A junior market only works if good companies keep using it — and for a stretch, they stopped. That’s the honest context behind the reforms below.

What changed in 2024 — and why it matters

To revive its fading junior board, the Hong Kong Stock Exchange rolled out a set of GEM listing reforms that took effect on 1 January 2024. As the law firm Morgan Lewis documented, the changes were aimed squarely at making the market usable again.

A few of the big moves:

- A new path for research-heavy companies. Firms investing seriously in R&D — at least HKD 30 million over two years, and 15% of their operating spend — can now list even without meeting the old cash-flow test. That’s a direct nod to modern tech and science startups that burn cash while they build.

- A shorter lock-up. The period controlling shareholders must hold their shares after listing was cut from 24 months to 12, matching the main board and improving how freely shares can trade.

- Lighter reporting. Quarterly financial reports became optional instead of mandatory, cutting compliance costs for smaller firms.

- An easier graduation. Companies moving up to the main board no longer need a costly sponsor-led due diligence process, provided they’ve spent three solid years as a GEM issuer.

The goal, in the exchange’s framing, was “revitalizing GEM” — reducing the cost and friction that had driven companies away, without throwing out the disclosure standards that protect investors.

So did the reforms work? (The 2025 reality check)

Honestly — not yet, or at least not fully. Just three companies listed on GEM in the whole of 2024, even after the rules were loosened, according to an April 2025 Hong Kong government update. There are flickers of life: GEM’s average daily turnover reached about HKD 78 million in March 2025, up 77% year-on-year, as liquidity slowly improved.

But a board that draws three listings a year is still a board in recovery. The lesson is sobering, and it’s the whole story of junior markets in miniature: you can cut the red tape, but you can’t force good companies to walk through the door — especially when investors are cautious and the wider mood is nervous. Reviving a junior market, it turns out, is far harder than reforming one.

What this means if you’re a founder

If you run a growing company, a Growth Enterprise Market is worth understanding as one option on a menu — not a default.

Going public early is a real tool. It can fund a growth push you couldn’t finance otherwise. But it comes with the cost, scrutiny, and reporting burden of being a public company, at a stage when your energy might be better spent on customers and product. The reputational baggage of some junior boards is real too — where you list becomes part of how the market and even how a business is classified and valued. For most companies, the practical path runs through private growth funding long before it reaches a stock exchange.

For most early-stage founders, private funding or simply growing on revenue will make more sense than a GEM listing. But for a specific kind of company — one with a genuine growth story, a need for larger capital than private markets will give, and the discipline to handle public reporting — it can be the right runway. The key is choosing it on purpose, eyes open, not because it sounds impressive.

Frequently Asked Questions

What is a Growth Enterprise Market in simple terms?

It’s a junior stock exchange board for smaller, younger, high-growth companies that can’t yet meet a main board’s strict profit and track-record rules. It lets them raise money from public investors earlier, in exchange for higher risk.

What’s the difference between GEM and the main board?

The main board is for large, established companies and demands a profit history and bigger size. A Growth Enterprise Market has lower entry requirements for smaller, unproven firms — which means easier access but more risk and often thinner trading.

Which exchanges have a Growth Enterprise Market?

The best-known is the Hong Kong Stock Exchange’s GEM. London’s equivalent is the Alternative Investment Market (AIM), and Kenya’s Nairobi Securities Exchange runs a Growth Enterprise Market Segment (GEMS). Many exchanges run a similar junior board under different names.

Is investing in Growth Enterprise Market companies risky?

Yes, generally more so than main-board stocks. GEM companies are younger and less proven, fail more often, and their shares can be harder to trade. The potential upside is earlier access to a growth story — but it comes with real downside risk.

The bottom line

A Growth Enterprise Market exists for a good reason: not every company that deserves capital fits the rigid mold of the main board. It’s the market’s way of saying “you’re not ready for the top league yet — but here’s a stage anyway.” That’s genuinely valuable, both for ambitious companies and for investors hunting early-growth stories.

Just don’t romanticize it. These boards carry real risk, real illiquidity, and a mixed track record — which is exactly why Hong Kong had to rebuild its own, and why even after the fix, only a trickle of companies have come. So the question isn’t whether a Growth Enterprise Market is good or bad. It’s whether your company is the specific kind that a junior board actually helps — or the kind that should wait, grow, and walk in the front door later.